Date:18/09/2023

In India, securing financing is a common necessity for various purposes, including buying a home, starting a business, funding education, or addressing unforeseen financial emergencies. When seeking loans, individuals have two primary options: secured loans and unsecured loans. Understanding the differences between these two types of loans is crucial to make informed financial decisions.

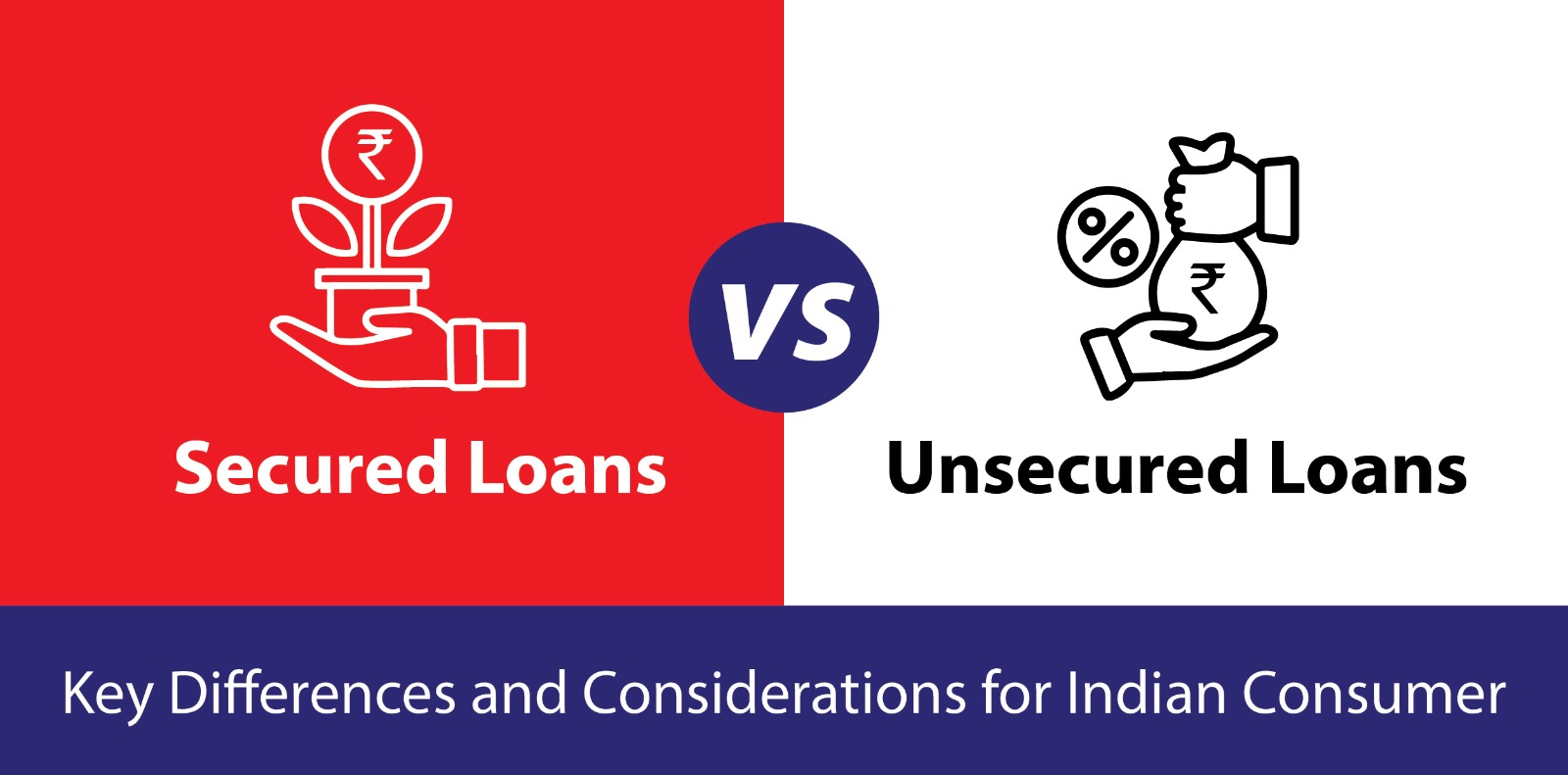

Secured Loans

Secured loans are backed by collateral, which is an asset that the borrower pledges to the lender as security for the loan. If the borrower fails to repay the loan, the lender can seize the collateral to recover the outstanding amount.

In India, common types of secured loans include:

Advantages:

Lower Interest Rates: Secured loans generally offer lower interest rates compared to unsecured loans because the lender has collateral as security.

Higher Loan Amounts: Lenders are willing to offer higher loan amounts due to reduced risk.

Longer Repayment Terms: Borrowers can often enjoy longer repayment tenures, making it easier to manage monthly instalments.

Risks:

Asset Risk: If you fail to repay the loan, you risk losing the collateral, which could be a valuable asset.

Eligibility Criteria: Secured loans often have strict eligibility criteria, including a good credit score and proof of collateral ownership.

Unsecured Loans

Unsecured loans do not require collateral, making them purely based on the borrower’s creditworthiness and ability to repay. Lenders assess the borrower’s financial history and income to determine eligibility.

Common unsecured loans in India include:

Advantages:

No Collateral Risk: Borrowers do not risk losing assets in case of non-payment.

Quick Approval: Unsecured loans often have faster approval processes.

Versatile Use: Can be used for various purposes, offering flexibility.

Risks:

Higher Interest Rates: Unsecured loans generally come with higher interest rates due to the increased risk for the lender.

Smaller Loan Amounts: Lenders may limit loan amounts, especially for those with lower credit scores.

Stricter Eligibility: Borrowers need a strong credit history and stable income to qualify for unsecured loans.

Factors to Consider When Choosing:

In conclusion, choosing between secured and unsecured loans in India depends on your specific financial situation and needs. Careful consideration of the advantages and risks associated with each type of loan will help you make the right choice and achieve your financial goals responsibly.

ABC of Gold Loans : Answering Your Common FAQs About Gold Loan

ABC of Gold Loans : Answering Your Common FAQs About Gold Loan

Plan Affordable Dream Weddings: How a Gold Loan Can Fund Your Dream Wedding ?

Plan Affordable Dream Weddings: How a Gold Loan Can Fund Your Dream Wedding ?

The Truth About Getting a Gold Loan with a Low CIBIL Score?

The Truth About Getting a Gold Loan with a Low CIBIL Score?

Instant Help for Farmers: How Money2Me Gold Loan Provides Quick Financial Support?

Instant Help for Farmers: How Money2Me Gold Loan Provides Quick Financial Support?

Gold Loans in the Digital Age: Convenience and Security at Your Fingertips

Gold Loans in the Digital Age: Convenience and Security at Your Fingertips

Gen Z’s Take on Gold Loans: Top 5 Myths Debunked

Gen Z’s Take on Gold Loans: Top 5 Myths Debunked

Can you apply for Gold Loan through online mode without visiting lenders place

Can you apply for Gold Loan through online mode without visiting lenders place

Reasons why Gold Loan is so inexpensive

Reasons why Gold Loan is so inexpensive

9 Reasons to opt for a Gold Loan, this Navratri Season.

9 Reasons to opt for a Gold Loan, this Navratri Season.

Gold Loan vs. Selling Gold: A Comprehensive Comparison

Gold Loan vs. Selling Gold: A Comprehensive Comparison